Savings Challenge: Your Path to Financial Freedom

Taking control of your finances can feel overwhelming, especially when your income is limited. Yet the desire to build a safety net, eliminate debt, or save for something meaningful remains strong. This is where a well-structured Savings Challenge becomes a game-changer. By breaking down a large goal into manageable, bite-sized steps, anyone can start saving consistently. The Low Income Savings Challenge Money Saving Challenge Bundle offers exactly this—a practical, portable, and motivational system designed for real-world budgets. Whether you're a student, a freelancer, a single parent, or someone just starting their financial journey, this bundle provides a clear roadmap. It transforms the abstract idea of saving into a tangible, daily habit that fits seamlessly into your life.

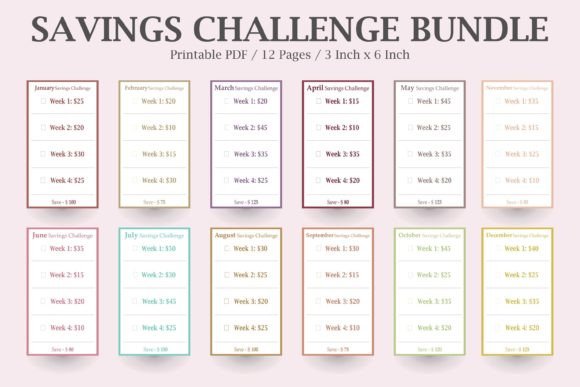

The core of this system lies in its simplicity. Instead of staring at a daunting annual target, you focus on a single monthly goal. Each month presents a fresh, achievable objective. For example, January might ask you to save $100, while February challenges you to save $75. These amounts are carefully calibrated to be realistic for those managing a tight budget. The bundle includes 12 distinct monthly challenges, ensuring variety and preventing monotony. You are not just saving money; you are engaging with a series of mini-adventures that keep you motivated. This approach is the essence of an effective Savings Challenge—it makes the process feel like a game rather than a chore.

Understanding the Low Income Savings Challenge Bundle

This isn't just a set of numbers on a page. It's a comprehensive Savings Bundle that includes dedicated trackers for each month. The design is intentionally minimalist, removing clutter so you can focus on what matters: your progress. Each tracker is an A6-sized printable, making it a perfect companion for your wallet, purse, or budget binder. The physical act of checking off a box or coloring in a section as you save creates a powerful visual reward. This tactile feedback reinforces your commitment and provides a sense of accomplishment that digital apps often lack.

The bundle is thoughtfully structured around the concept of mini challenges. Rather than one monolithic goal, you have multiple small victories throughout the year. This is particularly valuable for those using a Low Income Savings Challenge Money Saving Challenge Bundle, because it accommodates fluctuating cash flow. Some months you might save more, others less. The bundle's flexibility allows you to adjust without feeling like you've failed. You can even repeat a challenge if a particular month's goal proves too ambitious. The emphasis is always on progress, not perfection.

Who Benefits Most from This Approach?

While anyone can use this system, it is especially tailored for individuals who need structure but have limited financial flexibility. Consider the following scenarios:

- Students and part-time workers: Irregular income makes long-term planning hard. These mini challenges align with pay cycles and part-time hours.

- Single parents: Every dollar counts. Having a visual tracker helps involve the whole family in the savings goal, turning it into a shared activity.

- Freelancers and gig workers: Income variability means you need adaptable tools. The bundle's monthly format lets you save more during good months and less during lean ones.

- Those new to budgeting: If you've never saved before, starting small is key. The $75 or $100 goals feel achievable, building confidence for larger financial steps.

The Money-Saving Planner aspect of this bundle is not about restriction. It's about intentionality. You are deciding, in advance, where a portion of your money will go. This shifts your mindset from "I can't afford to save" to "I choose to save this much." That psychological shift is powerful. The bundle also integrates seamlessly with other financial tools like cash envelopes and budget binders, making it a versatile addition to your overall Money Management Kit.

Detailed Breakdown of the Monthly Challenges

Let's look at the specific challenges included. The bundle provides a clear structure for the entire year:

- January: Save $100 – A strong start to the year, setting a positive tone.

- February: Save $75 – A slightly lighter month, acknowledging shorter days and potential winter expenses.

- March: Save $125 – A push to build momentum as spring begins.

- April: Save $80 – Another manageable goal, perfect for tax season adjustments.

- May: Save $125 – Keeping the momentum going into mid-year.

- June: Save $100 – A balanced month as summer activities begin.

- July: Save $90 – Accommodating potential vacation or holiday spending.

- August: Save $110 – Preparing for back-to-school or end-of-summer expenses.

- September: Save $95 – A return to routine after summer.

- October: Save $105 – Building towards the holiday season.

- November: Save $85 – A lighter month before December.

- December: Save $70 – The smallest goal, recognizing higher holiday spending.

This structure demonstrates a deep understanding of real-world financial patterns. The amounts are not random; they reflect seasonal pressures and opportunities. By following this Frugal Savings Tracker, you could potentially save over $1,100 in a year—a significant sum for anyone on a low income. The key is consistency, not the amount. Each completed month builds financial discipline that lasts a lifetime.

Practical Ways to Use the Bundle in Daily Life

Integrating these trackers into your routine is straightforward. Here are some practical strategies:

- Pair with cash envelopes: Whenever you withdraw cash for groceries or gas, set aside a small amount in a designated savings envelope. Record it on your mini tracker.

- Use as a visual reminder: Place the current month's tracker inside your wallet or on your refrigerator. Each time you see it, you're reminded of your goal.

- Link to a specific purpose: Assign each month's savings to a particular goal—emergency fund, holiday gifts, a new appliance, or debt repayment. This adds emotional weight to the numbers.

- Celebrate milestones: When you complete a month's challenge, reward yourself in a small, non-financial way (like a walk in the park or a movie night at home). This reinforces positive behavior.

- Involve family: If you have children, let them help color in the tracker. It teaches them about saving in a concrete, visual way.

The Economic Savings Goals embedded in this bundle are designed to be realistic. They respect the financial constraints of low-income households while still encouraging growth. The bundle does not pretend that saving is easy. Instead, it provides a supportive framework that acknowledges challenges and celebrates small wins. This honest approach is what makes it effective.

Strengths of the Minimalist Low Income Savings Challenge Bundle

The bundle's minimalist design is one of its greatest strengths. There are no complicated graphs, no overwhelming spreadsheets, and no confusing jargon. It is a simple, clean tracker that anyone can use. This accessibility is crucial for those who may feel intimidated by traditional financial planning tools. The A6 size is also a deliberate choice. It is small enough to carry everywhere but large enough to read and update easily. It fits perfectly into standard A6 budget binder and cash envelopes, making it a cohesive part of a larger organizational system.

Another strength is its flexibility. You are not locked into a rigid annual plan. If you miss a month, you can simply start the next month's challenge. You can also rearrange the order of the challenges to match your personal cash flow. For example, if you know December is expensive, you could swap it with a lighter month. This adaptability makes the Savings Planner Bundle truly user-centric. It works for you, not the other way around.

Considerations and Practical Expectations

No financial tool is perfect for everyone, so it's important to set realistic expectations. This bundle is a tracking and motivational tool, not a magic solution. It will not create money out of thin air. You still need to have some disposable income, however small, to allocate toward savings. If your essential expenses exceed your income, no tracker can fix that. However, the bundle can help you identify areas where small savings are possible—perhaps by cutting one coffee run per week or opting for a cheaper streaming plan.

Some users may find that certain monthly goals are still too high. If that's the case, feel free to modify them. The spirit of the challenge is to save consistently, not to hit an arbitrary number. You can use the blank spaces on the trackers to set your own goals. The bundle is a template, not a prescription. Its true value lies in the habit it builds, not the exact dollar amounts.

Additionally, because these are printables, you need access to a printer and basic office supplies. For those who prefer digital tracking, you could import the PDFs into a note-taking app, but the physical format is where the magic happens. The act of writing and checking off is psychologically different from tapping a screen. If you are fully digital, you might need to adapt your approach.

Real-World Scenarios: How Different Users Benefit

Scenario 1: The Freelancer

Maria works as a freelance graphic designer. Her income fluctuates wildly month to month. She uses the Low Income Savings Challenge Money Saving Challenge Bundle to stay on track. In a good month, she completes two challenges. In a slower month, she focuses on just one smaller goal. The visual trackers give her a sense of control and progress, even when cash is tight. By the end of the year, she has saved enough to cover three months of basic expenses—a crucial safety net for her variable income.

Scenario 2: The New Parent

James and Priya are new parents adjusting to a single income. They use the bundle to save for their child's future. Each month, they commit to the challenge amount, even if it means eating out less or skipping a subscription. The mini trackers become a family activity. Their toddler loves putting stickers on the completed months. The bundle transforms saving from a stressful chore into a shared, joyful ritual.

Scenario 3: The Debt Repayer

Carlos is aggressively paying off credit card debt. He knows he needs to save simultaneously to avoid falling back into debt. He uses the bundle to build a small emergency fund while paying down his balance. The $70 to $125 monthly goals are achievable alongside his debt payments. After nine months, he has $800 saved and is debt-free. The bundle provided the structure he needed to balance two financial priorities.

Evaluating the Bundle for Your Needs

Before purchasing or downloading the Savings Bundle, ask yourself a few questions:

- Do I respond well to visual progress tracking?

- Am I looking for a simple, low-friction system?

- Do I need flexibility to adjust monthly goals?

- Am I motivated by small, frequent wins?

- Do I use a physical budget binder or cash envelopes?

If you answered yes to most of these, this bundle is likely a good fit. It is designed for people who want structure without complexity. It honors the reality that saving on a low income is hard, and it meets you where you are. The Affordable Budget Planner aspect ensures that you are not spending more on the tool than you will save using it. The digital download format keeps costs low while providing immediate access.

Long-Term Value and Habit Formation

The ultimate goal of any Savings Challenge is not just the money saved but the habit formed. By using this bundle for a full year, you train your brain to prioritize saving automatically. The monthly repetition creates a neural pathway that makes saving second nature. Future financial goals—whether building an emergency fund, saving for a home, or investing—become easier because you have already mastered the foundational skill of consistent saving.

Many users report that after completing the 12-month cycle, they continue using the trackers in subsequent years, often increasing the amounts. The bundle becomes a trusted companion in their financial journey. Its minimalist design means it never feels overwhelming. It is always there, quietly supporting your goals. This is the hallmark of a well-designed Money Management Kit: it fades into the background of your life while steadily building your financial resilience.

Final Thoughts on Your Savings Journey

Financial empowerment is not reserved for the wealthy. It is built through small, consistent actions. The Low Income Savings Challenge Money Saving Challenge Bundle embodies this principle perfectly. It breaks down a potentially intimidating goal into 12 friendly, manageable steps. It respects your reality while encouraging your growth. Whether you are saving for an emergency, a dream, or simply for peace of mind, this bundle provides the structure and motivation you need.

Remember, the best financial tool is the one you actually use. This bundle is designed to be used, not just admired. Its portability, simplicity, and flexibility make it a practical choice for anyone serious about improving their financial situation. Start with January's $100 challenge. Then February's $75. Build your momentum one month at a time. Before you know it, you will have created a habit that transforms your relationship with money forever. The journey of a thousand miles begins with a single step—or in this case, a single savings challenge.